20-F: Annual and transition report of foreign private issuers pursuant to Section 13 or 15(d)

Published on June 29, 2018

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) or (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended March 31, 2018 | |

| OR | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR | |

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 001-35776

Acasti Pharma Inc.

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

Québec, Canada

(Jurisdiction of incorporation or organization)

545, Promenade du Centropolis, Suite 100, Laval, Québec H7T 0A3

(Address of principal executive office)

Linda P. O’Keefe, Chief Financial Officer Acasti Pharma Inc.

545, Promenade du Centropolis, Suite 100 Laval, Québec H7T 0A3

Tel: 450-687-2262

Fax: 450-687-2272

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Name of each exchange on which registered | |

| Common Shares, no par value | The NASDAQ Capital Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

Not applicable

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

25,638,215 Common Shares issued and outstanding as of March 31, 2018.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ☐ Accelerated filer ☐ Non-accelerated filer ☐ Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ |

Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

TABLE OF CONTENTS

INTRODUCTION AND USE OF CERTAIN TERMS

As used in this annual report on Form 20-F, or this annual report, unless the context otherwise requires, references to “we”, “our”, “us”, “Acasti”, “Acasti Pharma”, “Corporation”, “it”, “its” or similar terms refer to Acasti Pharma Inc.

Market data and certain industry data and forecasts included in this annual report were obtained from internal company surveys, market research, publicly available information, reports of governmental agencies and industry publications and surveys. We have relied upon industry publications as our primary sources for third-party industry data and forecasts. Industry surveys, publications and forecasts generally state that the information they contain has been obtained from sources believed to be reliable, but that the accuracy and completeness of that information is not guaranteed. We have not independently verified any of the data from third-party sources or the underlying economic assumptions they made. Similarly, internal surveys, industry forecasts and market research, which we believe to be reliable based upon our management’s knowledge of our industry, have not been independently verified. Our estimates involve risks and uncertainties, including assumptions that may prove not to be accurate, and these estimates and certain industry data are subject to change based on various factors, including those discussed under “Risk Factors” in this annual report. While we believe our internal business research is reliable and the market definitions we use in this annual report are appropriate, neither our business research nor the definitions we use have been verified by any independent source. This annual report may only be used for the purpose for which it has been published.

We own or have rights to trademarks, service marks or trade names that we use in connection with the operation of our business. In addition, our name, logo and website names and addresses are our service marks or trademarks. CaPre® is our registered trademark. The other trademarks, trade names and service marks appearing in this annual report are the property of their respective owners. Solely for convenience, the trademarks, service marks, tradenames and copyrights referred to in this annual report are listed without the ©, ® and TM symbols, but we will assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks and tradenames.

Financial Information

All financial information in this annual report is presented in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB, unless otherwise specified.

We use multiple financial measures for the review of our operating performance. These measures are generally IFRS financial measures, but one adjusted financial measure, Non-IFRS operating loss (adding to net loss, finance expenses, depreciation and amortization and impairment loss, change in fair value of derivative warrant liabilities, stock-based compensation and by subtracting finance income and deferred income tax recovery), is also used to assess our operating performance. This non-IFRS financial measure is derived from our financial statements and is presented in a consistent manner. We use this measure, in addition to the IFRS financial measures, for the purposes of evaluating our historical and prospective financial performance, as well as our performance relative to competitors. All of these measures also help us to plan and forecast future periods as well as to make operational and strategic decisions. We believe that providing this Non-IFRS information to investors, in addition to IFRS measures, allows them to see our results through the eyes of our management, and to better understand our historical and future financial performance. See “Item 5. Operating and Financial Review and Prospects”, including for a reconciliation to net loss.

In this annual report, all references to “CA$” or “$” are to Canadian dollars, unless expressly otherwise stated. All amounts related to our financial results are presented in thousands of Canadian dollars, except where noted and per share amounts.

| - 1 - |

Exchange Rate Information

The following table presents the average exchange rate for one Canadian dollar expressed as one U.S. dollar for each of our last five fiscal years. The average rate is calculated using the average of the exchange rates on the last day of each month during the period.

| Fiscal Year Ended | Average | |||

| (US$) | ||||

| February 28,2014 | 0.9555 | |||

| February 28, 2015 | 0.8003 | |||

| February 29, 2016 | 0.7645 | |||

| March 31, 2017 | 0.7618 | |||

| March 31, 2018 | 0.7752 | |||

The following table presents the high and low exchange rate for one Canadian dollar expressed as one U.S. dollar for each month during the previous six months.

| Month | Low | High | ||||||

| (US$) | ||||||||

| November 2017 | 0.7759 | 0.7885 | ||||||

| December 2017 | 0.7760 | 0.7971 | ||||||

| January 2018 | 0.7978 | 0.8135 | ||||||

| February 2018 | 0.7807 | 0.8138 | ||||||

| March 2018 | 0.7641 | 0.7794 | ||||||

| April 2018 | 0.7747 | 0.7967 | ||||||

| May 2018 | 0.7680 | 0.7828 | ||||||

The exchange rates are based upon the daily average closing rate, as quoted by the Bank of Canada. As of June 28, 2018, the exchange rate for one Canadian dollar expressed as one U.S. dollar, as quoted by the Bank of Canada was $1.00 = US$0.7537.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains information that may be forward-looking information within the meaning of Canadian securities laws and forward-looking statements within the meaning of U.S. federal securities laws, both of which we refer to in this annual report as forward-looking information. Forward-looking information can be identified by the use of terms such as “may”, “will”, “should”, “expect”, “plan”, “anticipate”, “believe”, “intend”, “estimate”, “predict”, “potential”, “continue” or other similar expressions concerning matters that are not statements about the present or historical facts. Forward-looking information in this annual report includes, among other things, information or statements about:

| · | our ability to conduct all required clinical and nonclinical trials for CaPre, including the timing and results of those trials; |

| · | our strategy, future operations, prospects and the plans of our management; |

| · | the design, regulatory plan, timeline, costs and results of our clinical and nonclinical trials for CaPre; |

| · | the timing and outcome of our meetings and discussions with the U.S. Food and Drug Administration, or FDA; |

| · | our planned regulatory filings for CaPre, and their timing; |

| · | our expectation that our Bridging Study (as defined below) results will support our plan to get authorization from the FDA to use the 505(b)(2) pathway with new chemical entity, or NCE, status towards a New Drug Application, or NDA, approval in the United States; |

| · | the timing and results from two competitor outcomes studies in patients with high TGs (blood levels between 200-499 mg/dL); |

| · | the potential benefits and risks of CaPre as compared to other products in the pharmaceutical, medical food and natural health products markets; |

| · | our estimates of the size of the potential market for CaPre, unmet medical needs in that market, the potential for market expansion, and the rate and degree of market acceptance of CaPre if it reaches commercialization, and our ability to serve that market; |

| · | our anticipated marketing advantages and product differentiation of CaPre and its potential to become a best-in-class OM3 compound for the treatment of HTG; |

| · | the potential to expand CaPre’s indication for the treatment of high TGs (200-500 mg/dL); |

| · | the degree to which physicians would switch their patients to a product with CaPre’s target product profile; |

| · | our strategy and ability to develop, commercialize and distribute CaPre in the United States and elsewhere; |

| · | the manufacturing scale-up of CaPre beyond 20 tons and the related timing; |

| - 2 - |

| · | our ability to strengthen our patent portfolio and other means of protecting our intellectual property rights, including our ability to obtain additional patent protection for CaPre; |

| · | our expectation that following expiration of the license agreement with Neptune we will not require any license from third parties to support the commercialization of CaPre; |

| · | the availability, consistency and sources of our raw materials, including krill oil; |

| · | our expectation to be able to rely on third parties to manufacture CaPre whose manufacturing processes and facilities are in compliance with current good manufacturing practices, or cGMP; |

| · | the potential for OM3s in other cardiovascular medicine, or CVM, indications; |

| · | our intention and ability to build a US commercial organization and to successfully launch CaPre and compete in the US market; |

| · | our intention and ability to complete development and/or distribution partnerships to support the commercialization of CaPre outside of the US, and to pursue strategic opportunities to provide capital and market access; |

| · | our ability to reach a definitive agreement based upon a non-binding term sheet with a leading China-based pharmaceutical company for the commercialization of CaPre in certain Asian jurisdictions; |

| · | our need for additional financing and our estimates regarding our future financing and capital requirements; |

| · | our expectation regarding our financial performance, including our revenues, profitability, research and development, costs and expenses, gross margins, liquidity, capital resources, and capital expenditures; and |

| · | our projected capital requirements to fund our anticipated expenses, including our research and development and general and administrative expenses, and capital expenditures. |

Although the forward-looking information in this annual report is based upon what we believe are reasonable assumptions, you should not place undue reliance on that forward-looking information since actual results may vary materially from it. Important assumptions by us when making forward-looking statements include, among other things, assumptions by us that:

| · | we successfully and timely complete all required clinical and nonclinical trials necessary for regulatory approval of CaPre; |

| · | we successfully enroll and randomize patients in our TRILOGY Phase 3 program; |

| · | the timeline and costs for our clinical and nonclinical programs are not materially underestimated or affected by unforeseen circumstances; |

| · | CaPre is safe and effective; |

| · | outcome study data from two of our competitors in high HTG patients is positive; |

| · | we obtain and maintain regulatory approval for CaPre on a timely basis; |

| · | we are able to attract, hire and retain key management and skilled scientific personnel; |

| · | third parties provide their services to us on a timely and effective basis; |

| · | we are able to maintain our required supply of raw materials, including krill oil; |

| · | we are able to find and retain a third-party to manufacture CaPre in compliance with cGMP; |

| · | we are able to successfully build a commercial organization, launch CaPre in the US, and compete in the US market; |

| · | we are able to secure distribution arrangements for CaPre, if it reaches commercialization; |

| · | we are able to manage our future growth effectively; |

| · | we are able to gain acceptance of CaPre in its markets and we are able to serve those markets; |

| · | our patent portfolio is sufficient and valid; |

| · | we are able to secure and defend our intellectual property rights and to avoid infringing upon the intellectual property rights of third parties; |

| · | we are able to take advantage of business opportunities in the pharmaceutical industry and receive strategic partner support; |

| · | we are able to continue as a going concern; |

| · | we are able to obtain additional capital and financing, as needed; |

| - 3 - |

| · | there is no significant increase in competition for CaPre from other companies in the pharmaceutical, medical food and natural health product industries; |

| · | CaPre would be viewed favorably by payers at launch and receive appropriate healthcare reimbursement; |

| · | market data and reports reviewed by us are accurate; |

| · | there are no adverse changes in relevant laws or regulations; and |

| · | we face no product liability lawsuits and other proceedings or any such matters, if they arise, are satisfactorily resolved. |

In addition, the forward-looking information in this annual report is subject to a number of known and unknown risks, uncertainties and other factors, including those described in this annual report under the heading “Item 3.D. Risk Factors”, many of which are beyond our control, that could cause our actual results and developments to differ materially from those that are disclosed in or implied by the forward-looking information, including, among others:

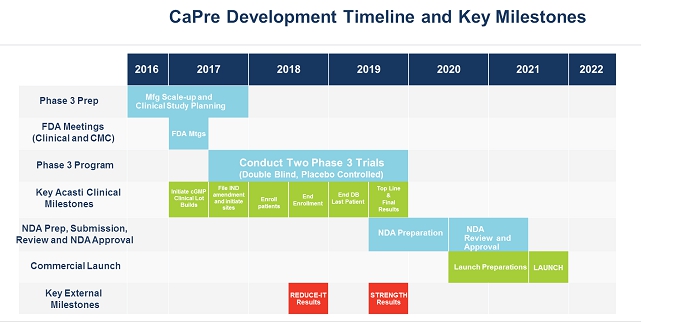

| · | risks related to timing and possible difficulties, delays or failures in our planned TRILOGY Phase 3 program for CaPre; |

| · | nonclinical and clinical trials may be more costly or take longer to complete than anticipated, and may never be initiated or completed, or may not generate results that warrant future development of CaPre; |

| · | CaPre may not prove to be as safe and effective or as potent as we currently believe; |

| · | our planned TRILOGY Phase 3 program may not produce positive results; |

| · | our anticipated studies and submissions to the FDA may not occur as currently anticipated, or at all; |

| · | the FDA could reject our 505(b)(2) regulatory pathway; |

| · | outcome study data from two of our competitors in high HTG patients may be negative, which could also negatively affect the market perception of CaPre; |

| · | we may encounter difficulties, delays or failures in obtaining regulatory approvals for the initiation of clinical trials or to market CaPre; |

| · | we may need to conduct additional future clinical trials for CaPre, the occurrence and success of which cannot be assured; |

| · | CaPre may have unknown side effects; |

| · | the FDA may refuse to approve CaPre, or place restrictions on our ability to commercialize CaPre; |

| · | CaPre could be subject to extensive post-market obligations and continued regulatory review, which may result in significant additional expense and affect sales, marketing and profitability; |

| · | we may fail to achieve our publicly announced milestones on time; |

| · | we may encounter difficulties in completing the development and commercialization of CaPre; |

| · | third parties we will rely upon to conduct our TRILOGY Phase 3 program for CaPre may not effectively fulfill their obligations to us, including complying with FDA requirements; |

| · | there may be difficulties, delays, or failures in obtaining health care reimbursements for CaPre; |

| · | recently enacted and future laws may increase the difficulty and cost for us to obtain marketing approval of and commercialize CaPre and affect the prices we can charge; |

| · | new laws, regulatory requirements, and the continuing efforts of governmental and third-party payors to contain or reduce the costs of healthcare through various means could adversely affect our business; |

| · | the market opportunity for, and demand and market acceptance of, CaPre may not be as strong as we anticipate; |

| · | third parties that we will rely upon to manufacture, supply and distribute CaPre may not effectively fulfill their obligations to us, including complying with FDA requirements; |

| · | there may not be an adequate supply of raw materials, including krill oil, in sufficient quantities and quality and to produce CaPre under cGMP standards; |

| · | Neptune still has some influence with respect to matters submitted to our shareholders for approval; |

| · | Neptune’s interest may not align with those of us or our other shareholders |

| - 4 - |

| · | we may not be able to meet applicable regulatory standards for the manufacture of CaPre or scale-up our manufacturing successfully; |

| · | we may not be able to produce clinical batches of CaPre in a timely manner or at all; |

| · | as a company, we have limited sales, marketing and distribution experience; |

| · | our patent applications may not result in issued patents, our issued patents may be circumvented or challenged and ultimately struck down, and we may not be able to successfully protect our trade secrets or other confidential proprietary information; |

| · | we may face claims of infringement of third party intellectual property and other proprietary rights; |

| · | we may face product liability claims and product recalls; |

| · | we face intense competition from other companies in the pharmaceutical, medical food and natural health product industries; |

| · | we have a history of negative operating cash flow and may never become profitable or be able to sustain profitability; |

| · | we have significant additional future capital needs and may not be able to raise additional financing required to fund further research and development, clinical studies, obtain regulatory approvals, build a commercial organization in the US, and meet ongoing capital requirements to continue our current operations on commercially acceptable terms or at all; |

| · | we may not be able to successfully compete in the US market with competitors who are larger and have more resources than we do; |

| · | we may acquire businesses or products or form strategic partnerships in the future that may not be successful; |

| · | we may be unable to secure development and/or distribution partnerships to support the development and commercialization of CaPre outside the US, provide development capital, or market access; |

| · | we rely on the retention of key management and skilled scientific personnel; and |

| · | general changes in economic and capital market conditions could adversely affect us. |

All of the forward-looking

information in this annual report is qualified by this cautionary statement. There can be no guarantee that the results or developments

that we anticipate will be realized or, even if substantially realized, that they will have the consequences or effects on our

business, financial condition or results of operations that we anticipate. As a result, you should not place undue reliance on

the forward-looking information. Except as required by applicable law, we do not undertake to update or amend any forward-looking

information, whether as a result of new information, future events or otherwise. All forward-looking information is made as of

the date of this annual report.

| - 5 - |

| Item 1. | Identity of Directors, Senior Management and Advisers |

Not applicable.

| Item 2. | Offer Statistics and Expected Timetable |

Not applicable.

| Item 3. | Key Information |

| A. | Selected Financial Data |

The following information should be read in conjunction with “Item 5. Operating and Financial Review and Prospects” and our audited financial statements and the related notes for our fiscal year ended March 31, 2018, which are prepared in accordance with IFRS as issued by the IASB and are included in this annual report. The selected financial information below includes financial information derived from our audited financial statements. Our historical results from any prior period are not necessarily indicative of results to be expected for any future period. The following table is a summary of our selected financial information in accordance with IFRS as issued by the IASB for each of our five most recently completed fiscal years.

| For the fiscal year ended | ||||||||||||||||||||

| March 31, 2018 | March 31, 2017 | February 29, 2016 | February 28, 2015 | February 28, 2014 | ||||||||||||||||

| Revenue from sales | $ nil | $ nil | $ nil | $ nil | $ | 501 | ||||||||||||||

| Loss from operating activities | $ | (19,696 | ) | $ | (11,210 | ) | $ | (9,612 | ) | $ | (12,395 | ) | $ | (10,800 | ) | |||||

| Net loss and total comprehensive loss | $ | (21,504 | ) | $ | (11,247 | ) | $ | (6,317 | ) | $ | (1,655 | ) | $ | (11,612 | ) | |||||

| Basic and diluted loss per share | $ | (1.23 | ) | $ | (1.01 | ) | $ | (0.59 | ) | $ | (0.16 | ) | $ | (1.38 | ) | |||||

| Total assets | $ | 22,959 | $ | 25,456 | $ | 28,517 | $ | 37,208 | $ | 45,632 | ||||||||||

| Total liabilities | $ | 14,735 | $ | 3,753 | $ | 1,297 | $ | 3,980 | $ | 12,352 | ||||||||||

| Share capital | $ |

73,338 |

$ | 66,576 | $ | 61,973 | $ | 61,628 | $ | 61,027 | ||||||||||

| Warrants and rights | $ | 715 |

$ | 453 | $ | — | $ | — | $ | 407 | ||||||||||

| Weighted average number of shares outstanding | 17,486,515 | 11,094,512 | 10,659,936 | 10,617,704 | 8,436,893 | |||||||||||||||

| Dividends declared per share | — | — | — | — | — | |||||||||||||||

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

Investing in our securities involves a high degree of risk due to, among other things, the nature of our business and the present stage of our development. Prospective and current investors should carefully consider the following risks and uncertainties, together with all other information in this annual report, as well as our financial statements included in this annual report and “Item 5. Operating and Financial Review and Prospects.” If any of these risks actually occur, our business, financial condition, prospects, results of operations or cash flow could be materially and adversely affected and you could lose all or a part of the value of your investment. Additional risks or uncertainties not currently known to us, or that we deem immaterial, may also negatively affect our business operations.”

General Risks Related to the Corporation

We may not be able to maintain our operations and advance our research and development of CaPre without additional funding.

We have incurred operating losses and negative cash flows from operations since our inception. To date, we have financed our operations through public offerings and private placements of securities, proceeds from exercises of warrants, rights and options, and receipt of research tax credits and research grant programs. Our cash and cash equivalents were $8.2 million as of March 31, 2018 and $9.8 million as of March 31, 2017.

| - 6 - |

Since our March 31, 2018 year end, the current assets have been increased by an incremental $10.0 million in approximate net proceeds from a May 2018 Canadian public financing, however, are projected to be less than needed to support our current liabilities as at that date when combined with the projected level of our expenses for the next twelve months, including the full initiation of clinical sites and ongoing enrollment of patients in, and the manufacturing of clinical materials for, our TRILOGY Phase 3 program for CaPre. Our positive working capital balance is expected to continue to decline until we raise additional funds. We will also require substantial additional funds to complete our TRILOGY Phase 3 program, obtain regulatory approvals and commercialize CaPre. In addition to completing nonclinical and clinical trials, we expect that additional time and capital will be required by us to file an NDA to obtain FDA approval for CaPre in the United States, to further scale up our manufacturing capabilities, and to complete marketing and other pre-commercialization activities. We will also most likely require additional capital to fund our daily operating needs. Based on a conservative estimate, we believe that our existing cash and cash equivalents will enable us to fund our operating expenses and capital expenditure requirements through September 2018. To fully execute our business plan, we will need to raise the additional necessary capital primarily through additional securities offerings and strategic alliances in the near term. We currently have no other arranged sources of financing. If we are unable to raise additional capital in sufficient amounts or on terms acceptable to us, we may have to significantly delay, scale back or discontinue our development or commercialization of CaPre or our other research and development initiatives. Delays or failures in our TRILOGY Phase 3 program for CaPre may affect our ability to complete strategic development and/or distribution partnerships to support the development and commercialization of CaPre. Additional funding from third parties may not be available on acceptable terms or at all to enable us to continue and complete our research and development of CaPre.

If we do not raise additional funds, we may not be able to realize our assets and discharge our liabilities in the normal course of business. As a result, there exists a material uncertainty that casts substantial doubt about our ability to continue as a going concern and, therefore, realize our assets and discharge our liabilities in the normal course of business. Our financial statements have been prepared on a going-concern basis, which assumes we will continue our operations in the foreseeable future and will be able to realize our assets and discharge our liabilities and commitments in the ordinary course of business. If we are unable to continue as a going concern, material write-downs to the carrying value of our assets, including intangible assets, could be required. If we fail to obtain additional financing, we may not be able to continue as a going concern.

We may never become profitable or be able to sustain profitability.

We are a clinical-stage biopharmaceutical company with a limited operating history. The likelihood of the success of our business plan must be considered in light of the problems, expenses, difficulties, complications and delays frequently encountered when developing and expanding early-stage businesses and the regulatory and competitive environment in which we operate. Biopharmaceutical product development is a highly speculative undertaking, involves a substantial degree of risk and is a capital- intensive business. We expect to incur expenses without any meaningful corresponding revenues unless and until we are able to obtain regulatory approval for and begin selling CaPre in significant quantities. We filed our investigational new drug application, or IND, for CaPre in late 2013, which allowed us to initiate clinical development in 2014 in the United States towards FDA approval for CaPre. To date, we have not generated any revenue from CaPre, and we may never be able to obtain regulatory approval for marketing CaPre in any indication. Even if we are able to commercialize CaPre, we may still not generate significant revenues or achieve profitability. Additionally, we may not be able to attain commercially viable cost of goods sold, and levels of insurance reimbursement for CaPre may not be commercially viable in all global markets. We incurred net losses for the fiscal year ended March 31, 2018 of $21.5 million, $11.2 million for the thirteen-month period ended March 31, 2017, and $6.3 million and $1.7 million for our fiscal years ended 2016 and 2015, respectively. As of March 31, 2018, we had an accumulated deficit of $72.4 million.

We expect that our expenses will increase significantly as we continue our Phase 3 clinical program for CaPre under the current indication and prepare to seek FDA approval for the commercial launch of CaPre. We also expect that our research and development expenses will continue to increase if we pursue FDA approval for CaPre for other indications. As a result, we expect to continue to incur substantial losses for the foreseeable future, and these losses may be increasing. We are uncertain about when or if we will be able to achieve or sustain profitability. If we fail to become and remain profitable, our ability to sustain our operations and to raise capital could be impaired and the price of our common shares could decline.

| - 7 - |

If outcome studies being conducted by two of our competitors testing the impact of OM3 on treating patients with high TGs are negative, there could also be an adverse impact for CaPre.

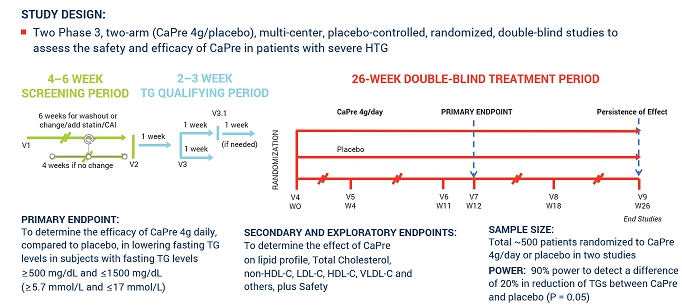

Two of our competitors are currently testing the effects of OM3 on patients with high TGs and taking statins concomitantly. These cardiovascular outcome studies are expected to report by the end of the third quarter of fiscal 2018 (the REDUCE-IT trial sponsored by Amarin) and in 2019 (the STRENGTH trial sponsored by AstraZeneca). If those studies show that OM3 therapeutic drugs effectively treat patients with high TGs and improve cardiovascular, morbidity and mortality outcomes, we believe that the potential to expand CaPre’s indication in the future to include the treatment of high TGs would be significantly advanced. Conversely, if outcome study data from one or both of those competitors is negative, or if one or both clinical trials fail to be completed, our potential target market for CaPre could be limited to patients with severe HTG (total global market was estimated by GOED Proprietary Research in 2015 to be approximately $2.3 billion) and our ability to realize greater market potential of CaPre could be harmed without conducting a successful outcomes trial with CaPre.

We will rely on third parties to conduct our TRILOGY Phase 3 program for CaPre.

We will rely on contract research organizations, or CROs, to monitor and manage data for our TRILOGY Phase 3 program for CaPre. While we will only control certain aspects of the CRO’s activities, we nevertheless are responsible for ensuring that our clinical trials are conducted in accordance with applicable protocols, and legal, regulatory and scientific standards, and our reliance on the CRO does not relieve us from those responsibilities. We and the CRO are required to comply with current good clinical practices, or cGCPs, which are regulations and guidelines enforced by the FDA, Health Canada and comparable foreign regulatory authorities for any products in clinical development.

The FDA enforces these cGCP regulations through periodic inspections of trial sponsors, principal investigators and trial sites. If we or the CRO fail to comply with applicable cGCPs, the clinical data generated in our clinical trials may be deemed unreliable and the FDA, Health Canada or comparable foreign regulatory authorities may require us to perform additional clinical trials before approving our marketing applications for CaPre. Upon inspection, the FDA could determine that our clinical trials do not comply with cGCPs. In addition, our clinical trials must be conducted with products produced under current good manufacturing practice, or cGMP, regulations and require a large number of test subjects. If we or the CRO fail to comply with these regulations, we may have to repeat preclinical studies or clinical trials for CaPre, which would delay the regulatory approval process and could also subject us to enforcement action up to and including civil and criminal penalties.

If our relationship with a CRO terminates, we may not be able to enter into arrangements with alternative CROs. If the CRO does not successfully carry out its duties or obligations or meet expected deadlines, if it needs to be replaced or if the quality or accuracy of the clinical data it obtains is compromised due to the failure to adhere to our clinical protocols, regulatory requirements or for other reasons, we may have to extend, delay or terminate our preclinical studies or clinical trials, and we may not be able to obtain regulatory approval for or successfully commercialize CaPre.

The third parties that will help conduct our TRILOGY Phase 3 program for CaPre will not be our employees and, except for remedies available to us under our agreements with the CROs, we cannot control whether or not they devote sufficient time and resources to our preclinical, clinical and nonclinical programs. These third parties may also have relationships with other commercial entities, including our competitors, for whom they may also be conducting clinical studies or other drug development activities, which could affect their performance on our behalf.

We rely on third parties to manufacture, produce and supply CaPre and we may be adversely affected if those third parties are unable or unwilling to fulfill their obligations, including complying with FDA requirements.

Producing pharmaceutical products requires significant expertise and capital investment, including the development of advanced manufacturing techniques and process controls. Currently, while we do own our manufacturing and encapsulation equipment, we do not own or operate manufacturing facilities for the production of CaPre. Accordingly, we need to rely on one or more third party contract manufacturers to produce and supply our required drug product for our nonclinical research and clinical trials for CaPre.

Although we are currently working with CordenPharma at its Chenôve facility in Dijon, France to scale up our manufacturing processes for CaPre, doing so is a difficult and uncertain task, and there are risks associated with scaling to the level required for full commercialization, including, among others, pricing, cost overruns, potential problems with process scale up, process reproducibility, stability issues, lot consistency and timely availability of reagents or raw materials. Consequently, we may not be able to attain our targeted cost of goods sold for CaPre. Any of these challenges could delay completion of our clinical trials or commercial launch of CaPre, require bridging or repetition of studies or trials, increase development costs, delay approval of CaPre, impair our commercialization efforts, and increase our costs. We may have to delay or suspend the production of CaPre if a third-party manufacturer:

| · | becomes unavailable for any reason, including as a result of the failure to comply with cGMP regulations; |

| - 8 - |

| · | experiences manufacturing problems or other operational failures, such as equipment failures or unplanned facility shutdowns required to comply with cGMP or damage from any event, including fire, flood, earthquake, business restructuring or insolvency; or |

| · | fails or refuses to perform its contractual obligations under its agreement with us, such as failing or refusing to deliver the quantities of CaPre requested by us on a timely basis. |

If our third-party contract manufacturers fail to achieve and maintain high manufacturing standards in compliance with cGMP regulations, we may be subject to sanctions, including fines, product recalls or seizures, injunctions, delays or suspensions of our clinical trials for CaPre, total or partial suspension of production of CaPre, civil penalties, withdrawals of previously granted regulatory approvals, and criminal prosecution. We do not currently have arrangements in place for redundant supply. If any one of our current contract manufacturers cannot perform as agreed, we may be required to replace that manufacturer. Although we believe that there are several potential alternative contract manufacturers who could manufacture CaPre, we may incur added costs and delays in identifying and qualifying any such replacement.

We depend on Neptune for certain administrative and accounting services.

Neptune has provided us in the past with certain shared back office services and functions, including corporate affairs, public company reporting, accounting, payroll, information technology, accounts payable, accounts receivable and shared premises. As of the date of this annual report, the corporate affairs, public company reporting, accounting, and accounts receivable services have not been renewed, and we are now incurring incremental costs to manage those functions independently ourselves. These additional costs are partially offset by reduced shared service fees, and we expect that these services will continue to be provided independently or through qualified third parties. If our arrangements with Neptune for the remaining services were to be terminated or not renewed, we may have to incur some additional costs to provide these services ourselves or to source them from another third party. We anticipate these operations to be fully independent of Neptune by the end of our 2019 fiscal year. However, there can be no assurances that this will fully materialize by such time. Currently, our arrangements with Neptune for the remaining services are on a month-to-month basis and can be terminated anytime by either Neptune or us.

We have historically had no marketing and sales organization and, as a company, no experience in marketing products. If we are unable to properly establish marketing and sales capabilities or enter into agreements with a strategic partner to market and sell CaPre, we may not be able to generate revenue.

We have historically had no sales, marketing or distribution capabilities and, as a company, we have also historically had no experience in marketing products. If CaPre or another of our future product candidates is approved for commercialization, unless we find a strategic partner to assist us with sales, marketing and distribution, we will be required to develop in-house marketing and sales force capability, which would require significant capital expenditures, management resources and time. Also, we would have to compete with other biotechnology and pharmaceutical companies to recruit, hire, train and retain marketing and sales personnel. We face competition in our search for strategic partners to assist us with sales, marketing and distribution, and we may not be able to establish or maintain any such arrangements. If we do find a strategic partner, any revenue we receive from CaPre would partly depend upon the efforts of that strategic partner, which may not be successful. We may have little or no control over the marketing and sales efforts by any strategic partner we find for CaPre and our revenue may be lower than if we had commercialized CaPre independently.

If we are not successful in attracting and retaining highly qualified personnel, we may not be able to successfully implement our business strategy.

Our ability to compete in the highly competitive pharmaceuticals industry largely depends upon our ability to attract and retain highly qualified managerial, scientific and medical personnel. Competition for skilled personnel in our market is intense and competition for experienced scientists may limit our ability to hire and retain highly qualified personnel on acceptable terms. We are highly dependent on our management, scientific and medical personnel. Despite our efforts to retain valuable employees, members of our management, scientific and medical teams may terminate their employment with us on short notice or, potentially, without any notice at all. The loss of the services of any of our executive officers or other key employees could potentially harm our business, operating results or financial condition. Our success may also depend on our ability to attract, retain and motivate highly skilled junior, mid-level, and senior managers and scientific personnel. In addition, we do not maintain “key person” insurance policies on the lives of our executives or those of any of our other employees. Other pharmaceutical companies with which we compete for qualified personnel have greater financial and other resources, different risk profiles, and a longer history in the industry than we do. They also may provide more diverse opportunities and better chances for career advancement. Some of these characteristics may be more appealing to high- quality candidates than what we can offer. If we are unable to continue to attract and retain high-quality personnel, the rate and success at which we can develop and commercialize CaPre and any other future product candidates would be limited.

| - 9 - |

Business disruptions could seriously harm our future revenue and financial condition and increase our costs and expenses.

Our operations, and those of our suppliers, third party manufacturers and other contractors and consultants could be subject to earthquakes, power shortages, telecommunications failures, water shortages, floods, hurricanes, typhoons, fires, extreme weather conditions, medical epidemics and other natural or man-made disasters or business interruptions, for which we are predominantly self- insured. The occurrence of any of these business disruptions could seriously harm our operations and financial condition and increase our costs and expenses. We rely on third-party manufacturers to manufacture CaPre. Our ability to obtain supplies of CaPre could be disrupted if the operations of our manufacturers and suppliers are affected by a man-made or natural disaster or other business interruption.

Our prospects currently depend entirely on the success of CaPre, which is still in clinical development, and we may not be able to generate revenues from CaPre.

We have no prescription drug products that have been reviewed or approved by the FDA, Health Canada or any similar regulatory authority. Our only prescription drug candidate is CaPre, for which we have not yet filed an NDA, and for which we must conduct a TRILOGY Phase 3 program, undergo further development activities and seek and receive regulatory approval prior to commercial launch, which we do not anticipate will occur until 2021 at the earliest. We have invested significant effort and financial resources in researching and developing CaPre. Further development of CaPre will require substantial investment, access to sufficient commercial manufacturing capacity and significant marketing efforts before we can generate any revenue from sales of CaPre, if it is ever approved for commercialization.

We do not have any other prescription drug candidates in development and so our business prospects currently depend entirely on the successful development, regulatory approval and commercialization of CaPre, which may never occur. Most prescription drug candidates never reach the clinical development stage and even those that do reach clinical development have only a small chance of successfully completing clinical development and gaining regulatory approval. If we are unable to successfully commercialize CaPre, we may never generate meaningful revenues. In addition, if CaPre reaches commercialization and there is low market demand for CaPre or the market for CaPre develops less rapidly than we anticipate, we may not have the ability to shift our resources to the development of alternative products.

If we encounter difficulties enrolling patients in our planned TRILOGY Phase 3 program, our development activities for CaPre could be delayed or otherwise adversely affected.

We may experience difficulties in patient enrollment in our clinical trials, including our planned TRILOGY Phase 3 program for CaPre, for a variety of reasons. Timely completion of our clinical trials in accordance with their protocols depends, among other things, on our ability to enroll a sufficient number of patients who remain in the trial until its conclusion. The enrollment of patients depends on many factors, including:

| · | the number of clinical trials for other product candidates in the same therapeutic area that are currently in clinical development, and our ability to compete with those trials for patients and clinical trial sites; |

| · | patient eligibility criteria defined in the protocol; |

| · | the size of the patient population; |

| · | the risk that disease progression will result in death before the patient can enroll in clinical trials or before the completion of any clinical trials in which the patient is enrolled; |

| · | the proximity and availability of clinical trial sites for prospective patients; |

| · | the design of the trial; |

| · | our ability to recruit clinical trial investigators with the appropriate competencies and experience; |

| · | our ability to obtain and maintain patient consents; and |

| · | the risk that patients enrolled in clinical trials will drop out of the trials before completion. |

Our planned TRILOGY Phase 3 program for CaPre may compete with other clinical trials for product candidates that are in the same therapeutic areas as CaPre. This competition could reduce the number and types of patients and qualified clinical investigators available to us, because some patients who might have opted to enroll in our TRILOGY Phase 3 program may instead opt to enroll in a trial being conducted by one of our competitors or a clinical trial site may not allow us to conduct our clinical program at that site if competing trials are already being conducted there. We may also encounter difficulties finding adequate clinical trial sites at which to conduct our TRILOGY Phase 3 program. Delays in patient enrollment may result in increased costs or may affect the timing or outcome of our planned TRILOGY Phase 3 program, which could impair or prevent its completion and adversely affect our ability to advance the development of CaPre.

| - 10 - |

We may not be able to obtain required regulatory approvals for CaPre.

We have limited experience in conducting and managing the clinical trials necessary to obtain regulatory approvals, including approval by the FDA and, as a company, we have no experience in obtaining approval of any product candidates. The research, testing, manufacturing, labeling, packaging, storage, sale, marketing, pricing, export, import and distribution of prescription drug products are subject to extensive regulation by the FDA and other regulatory authorities in the United States and other countries and those regulations differ from country to country. We are not permitted to market CaPre in the United States until we receive approval of an NDA from the FDA and similar restrictions apply in other countries. In the United States, the FDA generally requires the completion of preclinical testing and clinical trials of each drug to establish its safety and efficacy and extensive pharmaceutical development to ensure its quality before an NDA is approved. Regulatory authorities in other jurisdictions impose similar requirements. Of the large number of drugs in development, only a small percentage result in the submission of an NDA to the FDA and even fewer are approved for commercialization. To date, we have not submitted an NDA for CaPre to the FDA or comparable applications to other regulatory authorities.

Our receipt of required regulatory approvals for CaPre is uncertain and subject to a number of risks, including:

| · | the FDA or comparable foreign regulatory authorities or independent institutional review boards, or IRBs, may disagree with the design or implementation of our clinical trials; |

| · | we may not be able to provide acceptable evidence of the safety and efficacy of CaPre; |

| · | the results of our clinical trials may not meet the level of statistical or clinical significance required by the FDA or other regulatory agencies for marketing approval; |

| · | the dosing of CaPre in a particular clinical trial may not be at an optimal level; |

| · | patients in our clinical trials may suffer adverse effects for reasons that may or may not be related to CaPre; |

| · | we may be unable to demonstrate that CaPre’s clinical and other benefits outweigh its safety risks; |

| · | the data collected from our clinical trials may not be sufficient to support the submission of an NDA for CaPre or to obtain regulatory approval for CaPre in the United States or elsewhere; |

| · | the FDA or comparable foreign regulatory authorities may not approve the manufacturing processes or facilities of third party manufacturers with which we contract for clinical and commercial supplies of CaPre; and |

| · | the approval policies or regulations of the FDA or comparable foreign regulatory authorities may significantly change in a manner rendering our clinical data insufficient for approval. |

The FDA and other similar regulators have substantial discretion in the approval process and may refuse to accept our application or may decide that our data is insufficient for approval and require additional clinical trials, or preclinical or other studies for CaPre. If regulatory approval for CaPre is obtained in one jurisdiction that does not necessarily mean that CaPre will receive regulatory approval in all jurisdictions in which we seek approval. If we fail to obtain approval for CaPre in one or more jurisdictions, our ability to obtain approval in a different jurisdiction may be negatively affected.

Even if we receive regulatory approval for CaPre, it may just be for a limited indication.

If we obtain regulatory approval for CaPre, we will only be permitted to market it for the indication approved by the FDA, and any such approval may put limits on the indicated uses or promotional claims we may make for it, or otherwise not permit labeling that sufficiently differentiates CaPre from competitive products with comparable therapeutic profiles. For example, while our initial objective is to seek regulatory approval for the treatment of severe HTG, afterwards obtaining approval for CaPre to address mild to moderate HTG could greatly expand our potential market for CaPre. However, even if CaPre is approved for severe HTG, it may never be approved for the treatment of mild to moderate HTG. In addition, any approval we receive for CaPre could contain significant use restrictions for specified age groups, warnings, precautions or contraindications, or may be subject to burdensome post-approval study or risk management requirements. If any regulatory approval for CaPre contains significant limits, we may not be able to obtain sufficient funding or generate meaningful revenue from CaPre or be able to continue developing, marketing or commercializing CaPre.

We may be unable to find successful strategic partnerships to develop and commercialize CaPre.

We intend to seek co-development, licensing and/or marketing partnership opportunities with third parties that we believe will complement or augment our development and commercialization efforts for CaPre. Entering into partnership relationships may require us to incur non-recurring and other charges, increase our near and long-term expenditures, issue securities that dilute our existing shareholders or disrupt our management and business. Entering into partnership relationships could also delay the development of CaPre and our other future product candidates if we become dependent upon a strategic partner and that strategic partner does not prioritize the development of CaPre relative to its other development activities. In addition, we face significant competition in seeking strategic partners and the negotiation process is time-consuming and complex. We may not be successful in our efforts to establish a strategic partnership or other alternative arrangements for CaPre on our anticipated timeline, or at all, because CaPre may be deemed to be at too early of a stage of development for collaborative effort and third parties may not view CaPre as having the requisite potential to demonstrate safety and efficacy. Even if we do enter into strategic partnerships, those partnerships may not achieve our objectives.

We are currently engaged in strategic partnership discussions with several pharmaceutical companies for the development and commercialization of CaPre. On November 20, 2017, we announced the signing of a non-exclusive non-binding term sheet with a leading China-based pharmaceutical company, and discussions with other parties are proceeding. Completion of any transaction is subject to negotiation and execution of a definitive agreement, which if signed would grant an exclusive license to commercialize CaPre in certain Asian countries, including China. Any signed preliminary agreements are preliminary and non-binding at this stage and the license, upfront payment, possible milestone payments and royalties contemplated by them will only become operative if definitive documents are executed. While the negotiation process remains ongoing with the view to reach a definitive agreement, the outcome at this point in time is uncertain and it is possible that no definitive agreement will be reached, or, if a definitive agreement is reached, that its terms and conditions may differ from those in the preliminary agreements. If we do enter into definitive documents, the near-term timing of the next steps in the advancement of our research and development of CaPre could be affected as the development of CaPre in those Asian countries may have to be pursued under a separate clinical program from our North American TRILOGY Phase 3 program.

| - 11 - |

We may be unable to develop alternative product candidates.

To date, we have not commercialized any prescription drug candidates and, other than CaPre, we do not have any compounds in clinical trials, nonclinical testing, lead optimization or lead identification stages. If we fail to obtain regulatory approval for and successfully commercialize CaPre as a treatment for severe HTG or any other indication, whether as a stand-alone therapy or in combination with other treatments, we would have to develop, acquire or license alternative product candidates or drug compounds to expand our product candidate pipeline beyond CaPre. In such a scenario, we may not be able to identify and develop or acquire product candidates that prove to be successful products, or to develop or acquire them on terms that are acceptable to us.

We may not be able to compete effectively against our competitors’ pharmaceutical products.

The biotechnology and pharmaceutical industries are highly competitive. There are many pharmaceutical companies, biotechnology companies, public and private universities and research organizations actively engaged in the research and development of products that may be similar to CaPre. It is probable that the number of companies seeking to develop products and therapies similar to CaPre will increase. Many of these and other existing or potential competitors have substantially greater financial, technical and human resources than we do and may be better equipped to develop, manufacture and market products. These companies may develop and introduce products and processes competitive with or superior to CaPre. In addition, other technologies or products may be developed that have an entirely different approach or means of accomplishing the intended purposes of CaPre, which might render our technology and CaPre non-competitive or obsolete.

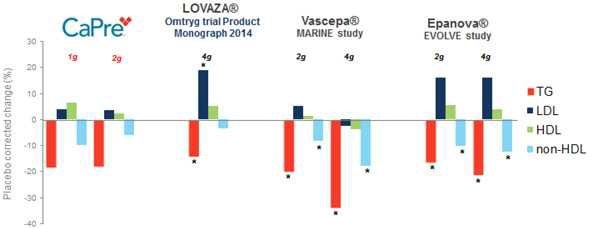

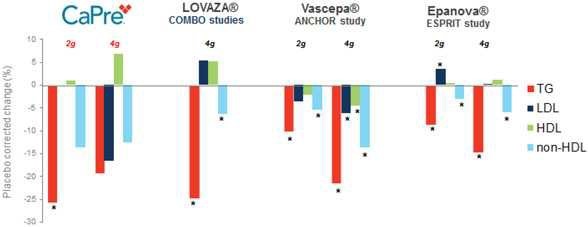

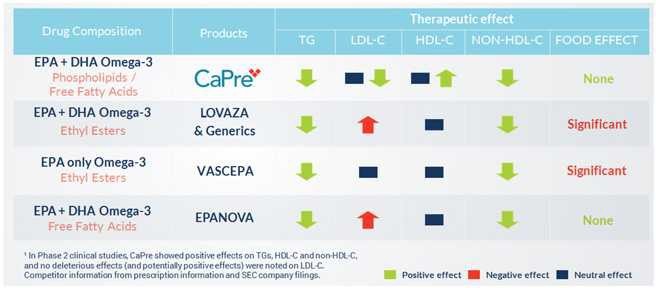

Our competitors in the United States and globally include large, well-established pharmaceutical companies, specialty pharmaceutical sales and marketing companies, and specialized cardiovascular treatment companies. GlaxoSmithKline plc, which currently sells LOVAZA, a prescription-only OM3 fatty acid indicated for patients with severe HTG, was approved by FDA in 2004 and has been on the market in the United States since 2005. Multiple generic versions of LOVAZA are now available in the United States. Amarin launched its prescription-only OM3 drug VASCEPA in 2013, and reached a market share of approximately 20% by the end of 2015. In addition, EPANOVA (OM3-carboxylic acids) capsules, a free fatty acid form of OM3 (comprised of 55% EPA and 20% DHA), is FDA-approved for patients with severe HTG. Omtryg, another OM3 fatty acid composition developed by Trygg Pharma AS, received FDA approval for severe HTG. Neither EPANOVA nor Omtryg have yet been commercially launched, but could launch at any time. Other large companies with products competing indirectly with CaPre include AbbVie, Inc., which currently sells Tricor and Trilipix for the treatment of severe HTG, and Niaspan, which is primarily used to raise HDL-C but is also used to lower TGs. Generic versions of Tricor, Trilipix and Niaspan are also now available in the United States. In addition, we are aware of a number of other pharmaceutical companies that are developing products that, if approved and marketed, would compete with CaPre.

Even if it receives regulatory approval, CaPre may need to demonstrate compelling comparative advantages in efficacy, convenience, tolerability and safety to be commercially successful. Other competitive factors, including generic drug competition, could force us to lower prices or could result in reduced sales of CaPre. In addition, new products developed by others could emerge as competitors to CaPre. If we are not able to compete effectively against our current and future competitors, our business will not grow and our financial condition and operations will suffer.

CaPre could face competition from products for which no prescription is required.

If it receives regulatory approval, CaPre will be a prescription-only OM3. Mixtures of OM3 fatty acids are naturally occurring substances in various foods, including fatty fish. OM3 fatty acids are also marketed by other companies as dietary supplements or natural health products. Dietary supplements may generally be marketed without a lengthy FDA premarket review and approval process and do not require a prescription. However, unlike prescription drug products, manufacturers of dietary supplements may not make therapeutic claims for their products; dietary supplements may be marketed with claims describing how the product affects the structure or function of the body without premarket approval, but may not expressly or implicitly represent that the dietary supplement will diagnose, cure, mitigate, treat, or prevent disease. We cannot be certain that physicians or consumers will view CaPre as superior to these alternatives or that physicians will be more likely to prescribe CaPre. If the price of CaPre is significantly higher than the prices of commercially available OM3 fatty acids marketed by other companies as dietary supplements or natural health products, physicians may recommend these commercial alternatives instead of CaPre or patients may elect on their own to take commercially available non-prescription OM3 fatty acids. Either of these outcomes could limit how we price CaPre and negatively affect our revenues.

Recent and future legal developments could make it more difficult and costly for us to obtain regulatory approvals for CaPre and negatively affect the prices we may charge.

In the United States and elsewhere, recent and proposed legal and regulatory changes to healthcare systems could prevent or delay our receipt of regulatory approval for CaPre, restrict or regulate our post-approval marketing activities, and adversely affect our ability to profitably sell CaPre. Proposals have also been made to expand post-approval requirements and to restrict sales and promotional activities for pharmaceutical products. We do not know whether additional legislative changes will be enacted, or whether the FDA’s regulations, guidance or interpretations will be changed, or what impact any such changes will have, if any, on our ability to obtain regulatory approvals for CaPre. Further, the Centers for Medicare and Medicaid Services, or CMS, frequently changes product descriptors, coverage policies, product and service codes, payment methodologies and reimbursement values. Also, increased scrutiny by the U.S. Congress of the FDA’s approval process could significantly delay or prevent our receipt of regulatory approval for CaPre and subject us to more stringent product labeling and post-marketing testing and other requirements.

| - 12 - |

In the United States, the Medicare Modernization Act, or the MMA, changed the way Medicare covers and pays for pharmaceutical products. The MMA expanded Medicare coverage for drug purchases by the elderly and introduced a new reimbursement methodology based on average sales prices for drugs. In addition, the MMA authorized Medicare Part D prescription drug plans to use formularies where they can limit the number of drugs that will be covered in any therapeutic class. As a result of the MMA and the expansion of federal coverage of drug products, we expect there will be additional pressure to contain and reduce healthcare costs. These healthcare cost reduction initiatives and other provisions of the MMA could decrease the coverage and price that we would receive for CaPre. While the MMA applies only to drug benefits for Medicare beneficiaries, private health insurance companies often follow Medicare coverage policy and payment limitations in setting their own reimbursement rates, and any reduction in reimbursement that results from the MMA may result in a similar reduction in payments from private health insurance companies.

The Patient Protection and Affordable Care Act, as amended by the Health Care and Education Affordability Reconciliation Act (the Health Care Reform Law), has broadened access to health insurance, reduced or constrained the growth of healthcare spending, enhanced remedies against fraud and abuse, added new transparency requirements for the healthcare and health insurance industries, imposed new taxes and fees on the health industry and imposed additional health policy reforms. Provisions of the Health Care Reform Law affecting pharmaceutical companies include requirements to offer discounts on brand-name drugs to patients who fall within the Medicare Part D coverage gap, commonly referred to as the “donut hole”, and to pay an annual non-tax deductible fee to the federal government based on each company’s market share of prior year total sales of branded products to certain federal healthcare programs, such as Medicare, Medicaid, Department of Veterans Affairs and Department of Defense.

Despite initiatives to invalidate the Health Care Reform Law, the U.S. Supreme Court has upheld key aspects of it. Due to the results of the recent presidential election, the Health Care Reform Law may be significantly changed and we do not know whether any such changes could have significant negative financial impact on the development or potential profitability of CaPre. At this time, it remains unclear whether there will be any changes made to the Health Care Reform Law, whether to certain provisions or its entirety. The Health Care Reform Law or any replacement of it could continue to apply downward pressure on pharmaceutical pricing, especially under the Medicare program, and may also increase our regulatory burdens and operating costs. Additional federal healthcare reform measures could be adopted in the future limiting the amounts that federal and state governments will pay for healthcare products and services, which could negatively affect the value of CaPre and our ability to achieve profitability.

In Canada, most new patented drug prices are limited so that the cost of therapy is in the range of the cost of therapy for existing drugs sold in Canada used to treat the same disease. As a result:

| · | prices of moderate and substantial improvement drugs and breakthrough drugs are also restricted by a variety of tests; |

| · | existing patented drug prices cannot increase by more than the Canadian Consumer Price Index; and |

| · | the Canadian prices of patented medicines can never be the highest in the world. |

If CaPre receives regulatory approval in Canada, restrictions on the price we can charge there for CaPre could reduce the value of CaPre and our ability to generate revenue and achieve profitability.

In many jurisdictions outside the United States, a product candidate must be approved for health care reimbursement before it can be approved for sale. In some cases, the price that we intend to charge for CaPre will also be subject to approval. If we fail to comply with the regulatory requirements in our target international markets or to receive required marketing approvals, our potential market for CaPre will be reduced and our ability to realize the full market potential for CaPre will be harmed.

Reimbursement decisions by third-party payors may have an adverse effect on pricing and market acceptance. If there is not sufficient reimbursement for CaPre, it is less likely that it will be widely used.

Even if CaPre is approved for sale by the appropriate regulatory authorities, market acceptance and sales of CaPre will depend on reimbursement policies and may be affected by future healthcare reform measures. Government authorities and third-party payors, such as private health insurers and health maintenance organizations, decide which drugs they will reimburse and establish payment levels. We cannot be certain that reimbursement will be available for CaPre. If reimbursement is not available or is available on a limited basis, we may not be able to successfully commercialize CaPre.

There may be significant delays in obtaining coverage and reimbursement for newly-approved drugs, and coverage may be more limited than the purposes for which the drug is approved by the FDA or other regulatory authorities. Moreover, eligibility for coverage and reimbursement does not imply that a drug will be paid for in all cases or at a rate that covers our costs, including research, development, manufacture, sale and distribution expenses. Interim reimbursement levels for new drugs, if applicable, may also be insufficient to cover our costs and may not be made permanent. Reimbursement rates may vary according to the use of a drug and the clinical setting in which it is used, may be based on reimbursement levels already set for lower cost drugs and may be incorporated into existing payments for other services. Net prices for drugs may be reduced by mandatory discounts or rebates required by government healthcare programs or private payors and by any future relaxation of laws that presently restrict imports of drugs from countries where they may be sold at lower prices than in the United States. Our inability to promptly obtain coverage and profitable payment rates from both government-funded and private payors for CaPre could have a material adverse effect on our operating results and our overall financial condition.

| - 13 - |

Even if we obtain FDA approval of CaPre, we may never obtain approval or commercialize it outside of the United States, which would limit our ability to realize CaPre’s full market potential.

In order to market CaPre outside of the United States, we must establish and comply with numerous and varying regulatory requirements of other countries regarding safety and efficacy. Clinical trials conducted in one country may not be accepted by regulatory authorities in other countries, and regulatory approval in one country does not mean that regulatory approval will be obtained in any other country. Approval procedures vary among countries and can involve additional product testing and validation and additional administrative review periods. Seeking foreign regulatory approvals could result in significant delays, difficulties and costs for us and may require additional preclinical studies or clinical trials, which would be costly and time consuming. Regulatory requirements can vary widely from country to country and could delay or prevent the introduction of CaPre in those countries. In addition, our failure to obtain regulatory approval in any country may delay or have negative effects on the process for regulatory approval in other countries. If we fail to comply with regulatory requirements in international markets or to obtain and maintain required approvals, our target market will be reduced and our ability to realize the full market potential of CaPre will be harmed.

If we or our third-party service providers fail to comply with healthcare laws and regulations or government price reporting laws, we could be subject to civil or criminal penalties.

In addition to the FDA’s restrictions on marketing pharmaceutical products, several other types of federal and state healthcare fraud and abuse laws restrict marketing practices in the pharmaceutical industry. These laws include the U.S. Anti-Kickback Statute, U.S. False Claims Act and similar state laws. The U.S. Anti-Kickback Statute prohibits, among other things, offering, paying, soliciting or receiving remuneration to induce, or in return for, purchasing, leasing, or ordering any healthcare item or service reimbursable under Medicare, Medicaid or other federally financed healthcare programs. A person or entity does not need to have actual knowledge of the U.S. Anti-Kickback Statute or special intent to violate the law in order to have committed a violation. This statute has been interpreted broadly to apply to arrangements between pharmaceutical manufacturers and prescribers, dispensers, purchasers and formulary managers. The exemptions and safe harbors from prosecution are drawn narrowly and we may fail to meet all of the criteria for safe harbor protection from anti-kickback liability.

In addition, the Health Care Reform Law provides that the government may assert that a claim including items or services resulting from a violation of the U.S. Anti-Kickback Statute constitutes a false or fraudulent claim for purposes of the U.S. False Claims Act. Federal false claims laws prohibit any person from knowingly presenting, or causing to be presented, a false claim for payment to the federal government or knowingly making, or causing to be made, a false statement to get a false claim paid. The “qui tam” provisions of the False Claims Act allow a private individual to bring civil actions on behalf of the federal government alleging that the defendant has submitted a false claim to the federal government. These individuals, sometimes known as “relators” or, more commonly, as “whistleblowers”, may share in any amounts paid by the entity to the government in fines or settlement. The number of filings of qui tam actions has increased significantly in recent years, causing more healthcare companies to have to defend a case brought under the federal False Claim Act. If an entity is determined to have violated the federal False Claims Act, it may be required to pay up to three times the actual damages sustained by the government, plus attorneys’ fees and costs, and civil penalties of up to US$21,563 for each separate false claim. Certain administrative sanctions, up to and including exclusion of an entity from participation in the federal healthcare programs, may also ensue.

Additional laws and regulations include:

| · | the U.S. federal Health Insurance Portability and Accountability Act (HIPAA), as amended by the Health Information Technology for Economic and Clinical Health Act (HITECH), which created additional federal criminal statutes that prohibit, among other things, schemes to defraud healthcare programs and imposes requirements on certain types of people and entities relating to the privacy, security, and transmission of individually identifiable health information, and requires notification to affected individuals and regulatory authorities of breaches of security of individually identifiable health information; |

| · | the federal Physician Payment Sunshine Act, which requires certain manufacturers of drugs, devices, biologics and medical supplies for which payment is available under Medicare, Medicaid, or the Children’s Health Insurance Program, to report annually to the CMS information related to payments and other transfers of value to physicians, other healthcare providers and teaching hospitals, and ownership and investment interests held by physicians and other healthcare providers and their immediate family members, which is published in a searchable form on an annual basis; and |

| - 14 - |

| · | the U.S. Foreign Corrupt Practices Act and similar worldwide anti-bribery laws, which generally prohibit companies and their intermediaries from making improper payments to government officials for the purpose of obtaining or retaining business. Violations of these laws, or allegations of such violations, could result in fines, penalties or prosecution and have a negative impact on our business, results of operations and reputation. |

Over the past few years, a number of pharmaceutical and other healthcare companies have been prosecuted under these laws for a variety of alleged prohibited promotional and marketing activities, such as providing free trips, free goods, sham consulting fees and grants and other monetary benefits to prescribers; reporting to pricing services inflated average wholesale prices that were then used by federal programs to set reimbursement rates; engaging in off-label promotion that caused claims to be submitted to Medicaid for non-covered, off-label uses; and submitting inflated best price information to the Medicaid Rebate Program to reduce liability for Medicaid rebates. Most states also have statutes or regulations similar to the U.S. Anti-Kickback Statute and the U.S. False Claims Act, which apply to items and services reimbursed under Medicaid and other state programs, or, in several states, apply regardless of the payor. Sanctions under these federal and state laws may include civil monetary penalties, exclusion of a manufacturer’s products from reimbursement under government programs, criminal fines and imprisonment. Settlements of U.S. government litigation may include Corporate Integrity Agreements with commitments for monitoring, training, and reporting designed to prevent future violations.